Answer a Few Questions

Complete our 2 minute quiz to review your top advisor matches.

You deserve an advisor you can trust. Find, hire, and invest with vetted, fiduciary financial advisors.

You deserve an advisor you can trust. Find, hire, and invest with vetted, fiduciary financial advisors.

You deserve an advisor you can trust. Find, hire, and invest with vetted, fiduciary financial advisors.

You deserve an advisor you can trust.

Find, hire, and invest with vetted, fiduciary financial advisors.

Complete our 2 minute quiz to review your top advisor matches.

Answer a Fes Questions

Complete our 2 minute quiz to review your top advisor matches.

Complete our 2 minute quiz to review your top advisor matches.

Interview vetted advisors to find the best fit.

Interview vetted advisors to find the best fit.

Interview vetted advisors to find the best fit.

Already have an advisor? Log In

Already have an advisor? Log In

Already have an advisor? Log In

Quickly open and fund your investment accounts in just minutes. Traditional platforms take weeks.

Securely access and effortlessly monitor your portfolio performance.

Securely access and effortlessly monitor your portfolio performance.

Quickly open and fund your investment accounts in just minutes. Traditional platforms take weeks.

Securely access and effortlessly monitor your portfolio performance.

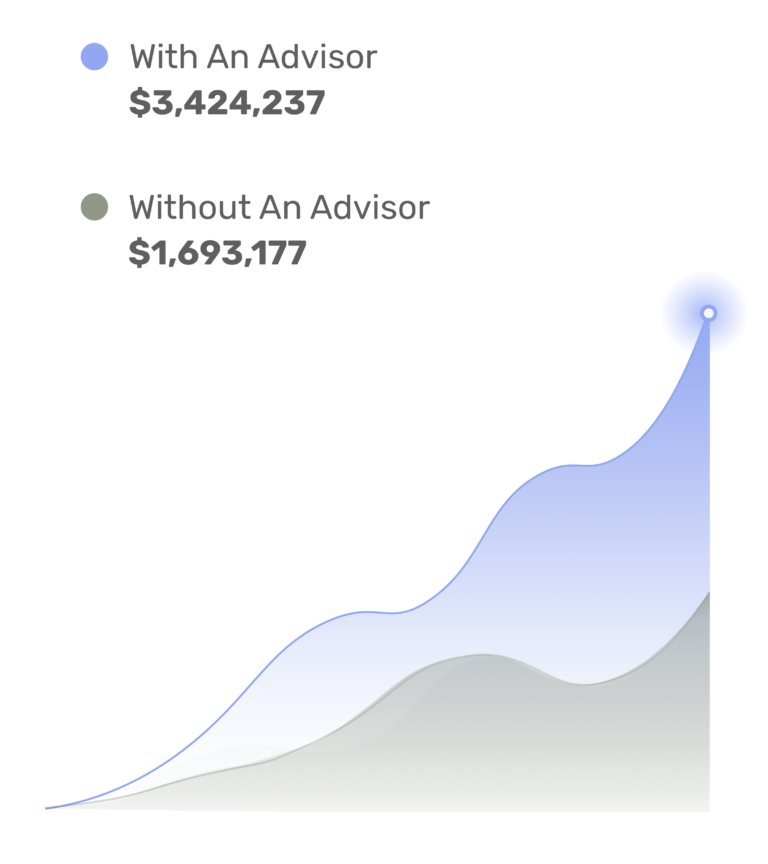

Working with an advisor can add as much as 3% more to your annual returns.

Working with an advisor can add as much as 3% more to your annual returns.

25-Year Investment**

25-Year Investment**

Working with an advisor can add as much as 3% more to your annual returns.

25-Year Investment**

“The quality of the referrals were top notch, the choices were good enough that the final decision was subjective.”

“Partnering with Zoe has allowed us to onboard clients & deliver the best service in a frictionless way.”***

The preceding testimonials are provided by current clients. Advisor does not seek out client testimonials, and all testimonials referenced are unsolicited. No compensation was provided for the testimonial and no material conflicts of interest are present as a result. These testimonials and endorsements do not guarantee a level of success, nor do they guarantee that all clients will have the same experience.

“Partnering with Zoe has allowed us to onboard clients & deliver the best service in a frictionless way.”***

The preceding testimonials are provided by current clients. Advisor does not seek out client testimonials, and all testimonials referenced are unsolicited. No compensation was provided for the testimonial and no material conflicts of interest are present as a result. These testimonials and endorsements do not guarantee a level of success, nor do they guarantee that all clients will have the same experience.

The preceding testimonials are provided by current clients. Advisor does not seek out client testimonials, and all testimonials referenced are unsolicited. No compensation was provided for the testimonial and no material conflicts of interest are present as a result. These testimonials and endorsements do not guarantee a level of success, nor do they guarantee that all clients will have the same experience.

* Best Online Financial Advisor is a rating given by NerdWallet for the calendar years ’22 and ’23, based on several criteria to compare companies that provide financial planning services online or connect users with a financial advisor. Most Innovative Companies is a rating given by Fast Company for the calendar year ’22, recognizing the organizations that are transforming industries and shaping society. Find more information on FastCompany Awards, Nerdwallet Awards, and additional disclosures here. **Assuming 5% annualized growth of 500k portfolio vs 8% annualized growth of advisor-managed portfolio over 25 years. ***“The endorsement was provided by an unaffiliated non-client. Zoe does not seek out endorsements, and all endorsements referenced are unsolicited. No compensation was provided for the endorsement however a conflict of interest does exist as this person is on the Zoe network as an available Advisor, and may be an option for clients to choose. This creates a conflict of interest because the advisor has financial incentive to speak highly of Zoe due to being compensated by clients who choose to work directly with them. These endorsements do not guarantee a level of success, nor do they guarantee that all clients will have the same experience.

* Best Online Financial Advisor is a rating given by NerdWallet for the calendar years ’22 and ’23, based on several criteria to compare companies that provide financial planning services online or connect users with a financial advisor. Most Innovative Companies is a rating given by Fast Company for the calendar year ’22, recognizing the organizations that are transforming industries and shaping society. Find more information on FastCompany Awards, Nerdwallet Awards, and additional disclosures here. **Assuming 5% annualized hypothetical growth of 500k portfolio vs 8% hypothetical annualized growth of advisor-managed portfolio over 25 years. Source: Putting a value on your value: Quantifying Vanguard Advisor’s Alpha, Vanguard, July 2022. ***“The endorsement was provided by an unaffiliated non-client. Zoe does not seek out endorsements, and all endorsements referenced are unsolicited. No compensation was provided for the endorsement however a conflict of interest does exist as this person is on the Zoe network as an available Advisor, and may be an option for clients to choose. This creates a conflict of interest because the advisor has financial incentive to speak highly of Zoe due to being compensated by clients who choose to work directly with them. These endorsements do not guarantee a level of success, nor do they guarantee that all clients will have the same experience.

Disclosure: This page is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accounting, tax, legal or financial advisors. The observations of industry trends should not be read as recommendations for stocks or sectors.