There is nothing quite as awful as a bad surprise. Be it an emergency, taxes, or a rate increase – why is it that unpleasant surprises are usually costly? Often, the blame can be placed on a lack of clarity and timely planning.

Lately, we’ve heard from investors that this tax season has been “extra frustrating.” For those who are feeling the burn of costly taxes due to their investments, the best way to avoid future sticker shock is to prepare. The first step towards decreasing taxes is to be aware of where those costs originate. That’s where investment tax rates come into play: while tax rates should not be the determining factor in your investment strategy, understanding them can help to know what you’ll be dealing with come tax time!

Breaking Down Investment Taxes

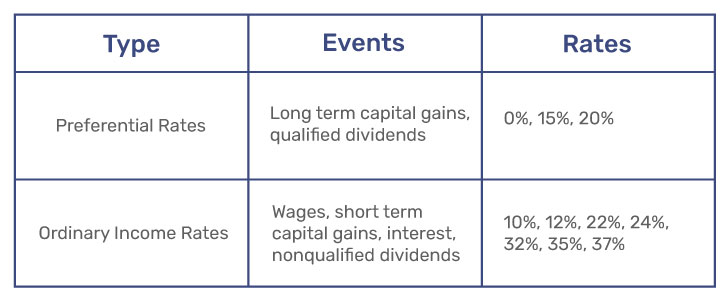

Investment tax rates are the taxes you will owe on income from your investments. The federal government taxes both investment income (dividends, interest, and rent), as well as capital gains. There are two main types of tax rates associated with these taxes: preferential rates and ordinary income rates.

Preferential rates mean the money being taxed has a preferred source, holding period, or purpose according to the IRS. Long-term capital gains and qualified dividends are taxed at preferential rates of either 0%, 15%, or 20%. In addition, you could potentially owe a 3.8% surtax on net investment income. You’ll only owe the surtax if your investment income and your modified adjusted gross income go over a certain amount.

Ordinary income rates, on the other hand, are the normal rate at which most income is taxed. In addition to wages, your short-term capital gains, interest, and non-qualified dividends are subject to ordinary income tax. Finally, you could be subject to the alternative minimum tax (AMT). This is triggered when taxpayers have more income than an exemption amount and they make use of many common itemized deductions.

When Do These Different Investment Tax Rates Come Into Play?

As discussed above, investment taxes can occur upon the sale of a position, as well as from ongoing dividends, interest, or fund distributions. Here is how these tax rates come into play depending on the type of income gained from your investment.

Capital Gain Taxes

When you sell a capital asset (like a stock, bond, or investment property) the sale price minus what you paid for it will equal the gain or loss. Whether the position is taxed at ordinary income (short term rates) or preferential rates (long term rates) will depend on how long you held the asset.

If your asset is held for less than one year, then it is short-term. Keep in mind that if your asset is held for one year or longer then it will be taxed at long-term rates.

Dividends

A dividend is a piece of a company’s profits paid to shareholders. For tax purposes, there are two kinds of dividends: qualified or nonqualified.

Qualified dividends are given the benefit of preferential tax rates. The IRS has certain requirements to be considered ‘qualified’ but don’t worry your investment custodian will tell you if you qualify. If your dividend does not match these terms then it is nonqualified and taxed at ordinary income rates.

Interest

Most interest income earned on investments is taxable as income at both the federal and state level. This includes the interest you earn from: CDs, US savings and treasury bonds, corporate bonds, checking and savings accounts, money market accounts, and interest income from pass-through businesses.

The main exception for tax-exempt interest is on municipal bonds. The interest is exempt from federal taxes but may not be exempt from state and local taxes depending on the municipality

Mutual Fund and ETF Distributions

Mutual funds and ETFs pay out distributions to all of their shareholders. As a reminder, mutual funds and ETFs are both investment products that have underlying stocks, bonds, and/or commodities.

When there is trading within the fund, it will create capital gains which then have to be paid out to the shareholders. These distributions are taxable to you even though you haven’t made any changes. The good news is that if you are automatically reinvesting, these distributions will be added to your cost basis so they will not be taxed twice.

Preempt a Bad Surprise: Investment Tax Strategy Next Steps

After reading about how various tax rates come into play, you may be thinking, “knowledge is power, but now what?”

While the rates your investments may be taxed under shouldn’t be deciding factor in how you might invest, having a baseline understanding can help you steer clear of unpleasant surprises. The next step is to begin developing a tax strategy. Tax planning analyzes your finances, assets, and liabilities to determine where you might optimize your taxes in the short and long term. As you’re likely realizing, there are plenty of variables that come into play!

From implementing a robust tax-loss harvesting strategy to introducing charitable tax distributions or evaluating tax credits you may not be considering currently, the best way to integrate tax-efficient strategies alongside your investment strategy is by speaking to an expert.