You know how it goes – life is about change. Whether on a personal level or due to external factors, we are consistently subject to change. This year has been particularly notable in its ever-changing nature. The real estate landscape, for one, has shifted dramatically over the past year. For much of the past twelve months, the combination of rock bottom rates and low inventory led to stiff competition for homes.

From another lens, the Federal Reserve has increased rates to combat rising inflation levels, which translates to higher mortgage rates. Despite several interest rate hikes, housing prices have largely continued their upward trajectory. Now with prices still on the rise, interest rates are at their highest point since the Great Recession.

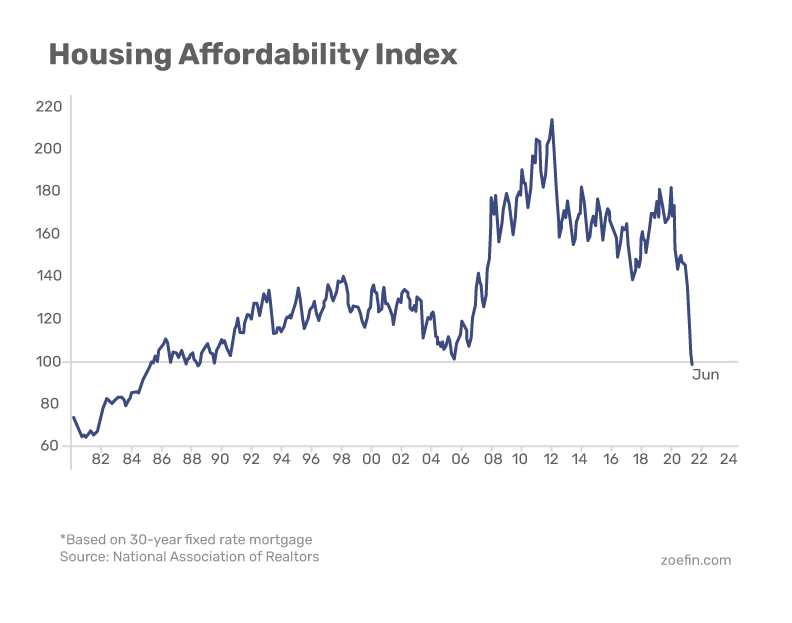

Housing affordability had dropped to levels not seen since 2006 due to inadequate inventory. But the frenzy of home price increases seems to be finally cooling with reports highlighting the first decrease in US home values since 2012.

While there are external changes you can’t control, there are times when it makes sense to take change into your own hands! If you are in the market for a new home, now could be a good time to evaluate the evolving housing climate. Let’s take a moment to explore several factors that will impact your decision.

The Big One: Mortgage Payments

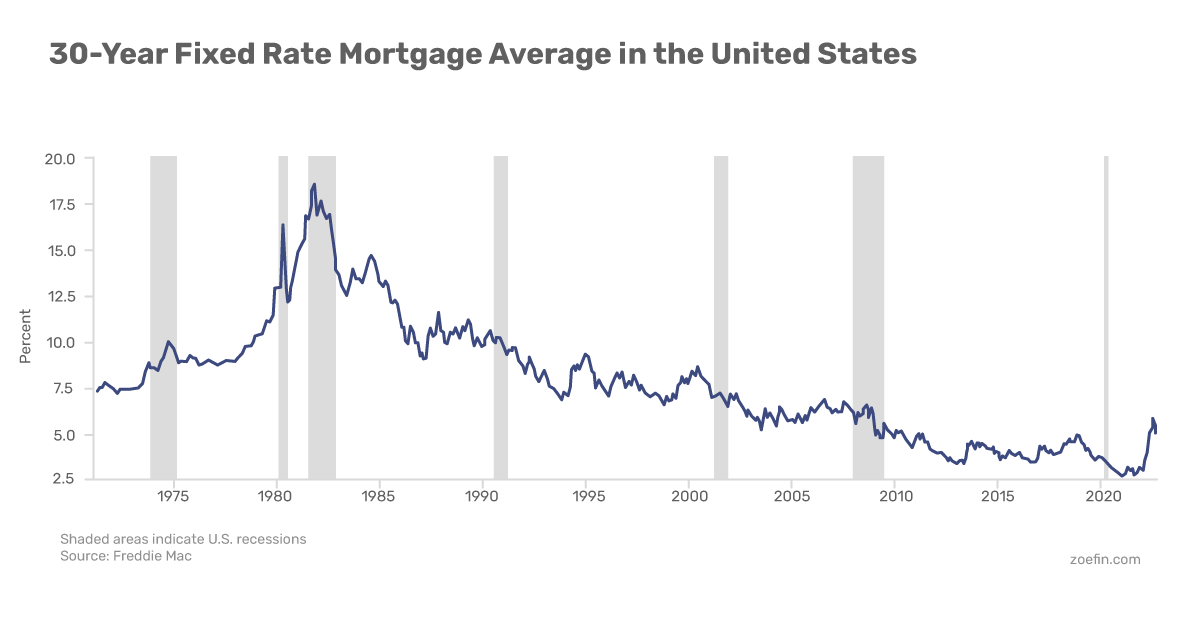

According to Freddie Mac’s Primary Mortgage Market Survey, the U.S. entered 2022 with an average rate on a 30-year fixed mortgage of 3.11%. By the week ending August 18th 2022, that figure had climbed to 5.13%. A difference of 2.02% in your interest rate may seem small, but it makes a big impact when calculating your monthly mortgage payment.

Here is an example: a borrower financing $500,000 at 3.11% is looking at a monthly payment of $2,138 in principal and interest. At 5.13% that payment jumps to $2,724 – an increase of over 27%. Increased rates have led many buyers to lower their target purchase price or eliminate themselves from the housing market entirely.

Yet despite rising mortgage rates, they are still historically low (as seen on the chart below). It may still be a good time to fix your housing payment for the long run as opposed to renting – which itself is not immune to inflation.

If you are a serious buyer, getting pre-approval from a mortgage lender will put you in the best position to understand your potential payment and the full range of costs you can expect as part of buying a house. There are also many quality online mortgage payment calculators that can help give you a sense of your monthly payment depending on the details of your prospective home.

‘Competition’ Might Have a Positive Connotation

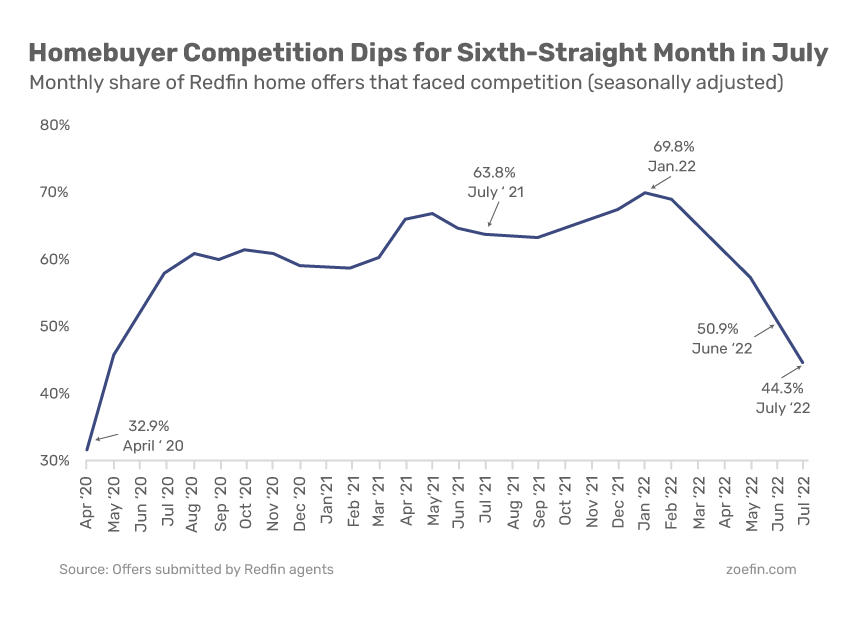

If you are in the market for a new home, increased rates may work to your benefit. As rates have gone up, competition has decreased. At the beginning of the year, it was the norm to hear about houses receiving dozens of offers and selling for well over the asking price. Those days may largely be over.

Redfin tracks the share of home offers that face competition. After the peak in January, that rate declined for the following months. Competition is now approaching pre-pandemic levels. Less competition means buyers have more leverage to negotiate contract terms and the sales price.

Home Values and Supply

The frenzy of home price increases seems to be cooling. According to Redfin data, properties are staying on the market for longer and more sellers are responding by slashing prices. Over 8% of Redfin listings saw a price drop in the month of July.

Part of what drove prices up in the first place was a housing supply shortage. Despite some sellers choosing to hang onto their properties instead of selling, we are now seeing increases in the overall housing supply. The total number of homes for sale is up 4% yearly. Zillow reports the first decrease in US home values since 2012, making it clear that there is an impact.

A cooling market can give home buyers the flexibility to find the right property for them on the right terms.

How Should You Respond?

Though the broader real estate market trends will impact your ability to buy a home, the decision must ultimately make sense within the context of your personal financial plan. Your readiness may not perfectly align with ideal conditions in the market, but if you consider these three factors, you can put yourself in a position to succeed:

- Maintain about 3-6 months of your spending as an emergency reserve. Before buying a house, increase cash savings to account for your higher housing costs (if applicable) as well as any unexpected costs that may come as a result of home ownership.

- Qualifying for a certain mortgage does not mean you should jump into it. Ensure that your new mortgage payment fits into your budget. Not sure? Test it out by saving your new mortgage payment into a savings account for a few months.

- Buying a house should be a long-term decision. If you plan to own the property long term, you reduce the frictional costs associated with buying/selling such as agent and transfer fees, as well as reducing the risk of having to sell after buying at the market’s peak. Plus, more time in your home translates to more opportunities to build equity over the long term.

If you are wondering how buying a home impacts your financial plan, finding the right advice can help. Change includes uncertainty and a financial advisor who understands your background and goals can be the best addition to your future planning.