Find Your Fiduciary Financial Advisor

You deserve an advisor you can trust. Let us connect you with an independent, fiduciary financial advisor.

Find An Advisor

How It Works

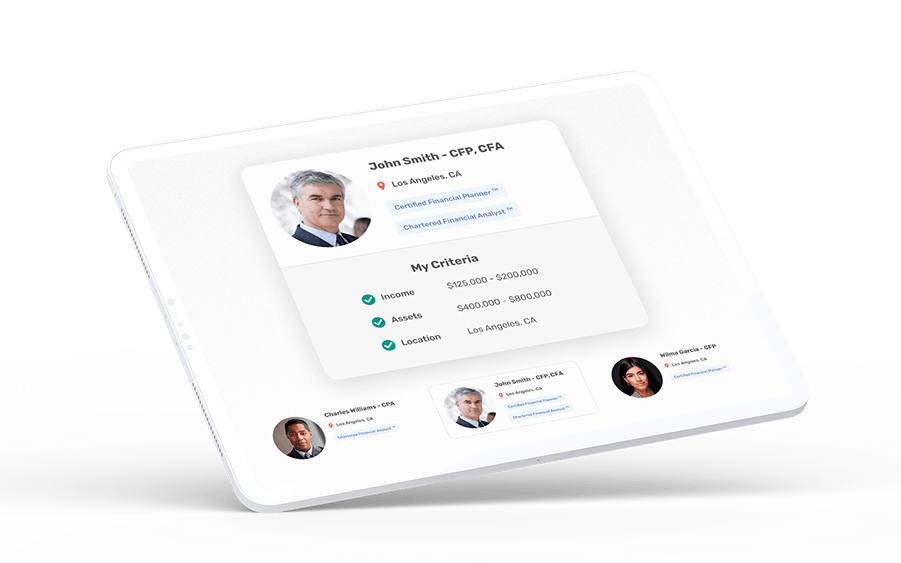

Get Matched

Our algorithm handpicks the fiduciary financial advisor best suited to your unique situation.

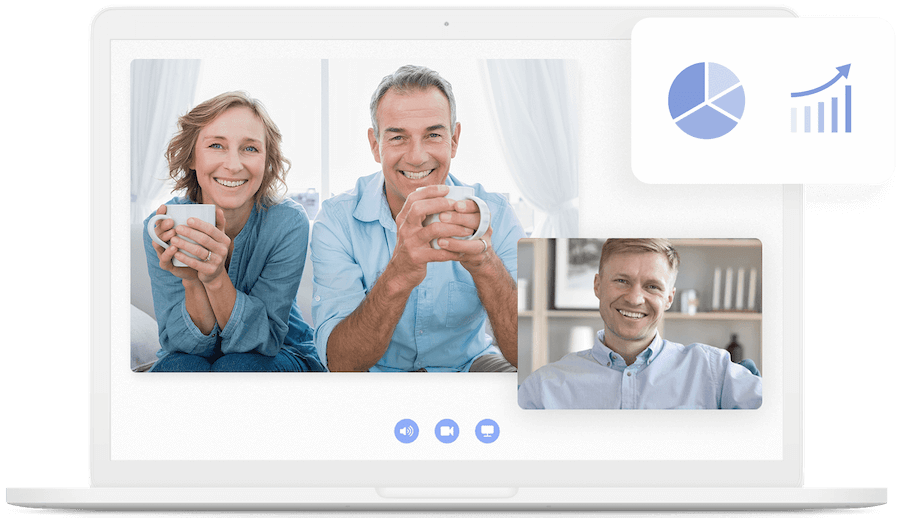

Have a Conversation

Connect with your advisor matches

and find the right fiduciary financial advisor for you.

Start Your Growth

Build a relationship with a trusted expert

and secure your financial future.